Should I sell or rent my house? If you locked in a mortgage rate of 3% or 4%, that question deserves a careful answer. At 1836 Property Management, we have managed Austin rentals since 2007, and today we care for more than 900 homes valued at over $300 million across the Austin area. We have also partnered with Austin's top real estate companies, so we see both sides of this decision every week. In our experience, a low mortgage rate is one of the most valuable financial assets a homeowner can hold. Selling gives it up for good. Renting lets you keep it working for you. Below, we walk through the real math so Austin homeowners can decide with confidence.

Key Takeaways

- Your low mortgage rate is tied to your loan, not your house, so you can rent your home out and keep the rate.

- Replacing a 3% or 4% loan today costs far more, since the average 30-year rate now sits near 6.5%.

- Selling is expensive and final. It can cost around $30,000 and ends your rate advantage for good.

- Charging the same rent, a low-rate owner keeps about $590 more each month, or roughly $7,080 a year.

- Renting can build wealth three ways: your tenant pays down the loan, the home may appreciate, and you may qualify for tax deductions.

- Selling still makes sense in some cases, such as low equity, major repairs, or not wanting to be a landlord.

- A property manager can handle pricing, tenants, and maintenance, so keeping your home stays hands-off.

Table of Contents

- What Is the Mortgage Rate Lock-In Effect?

- Should I Sell or Rent My House? Look at the Real Numbers

- Rent vs Sell House: A Side-by-Side Example

- When Does Selling Still Make More Sense?

- How Do You Turn Your Home Into a Rental Property?

- Let a Property Manager Handle the Hard Part

- Frequently Asked Questions

- The Bottom Line

What Is the Mortgage Rate Lock-In Effect?

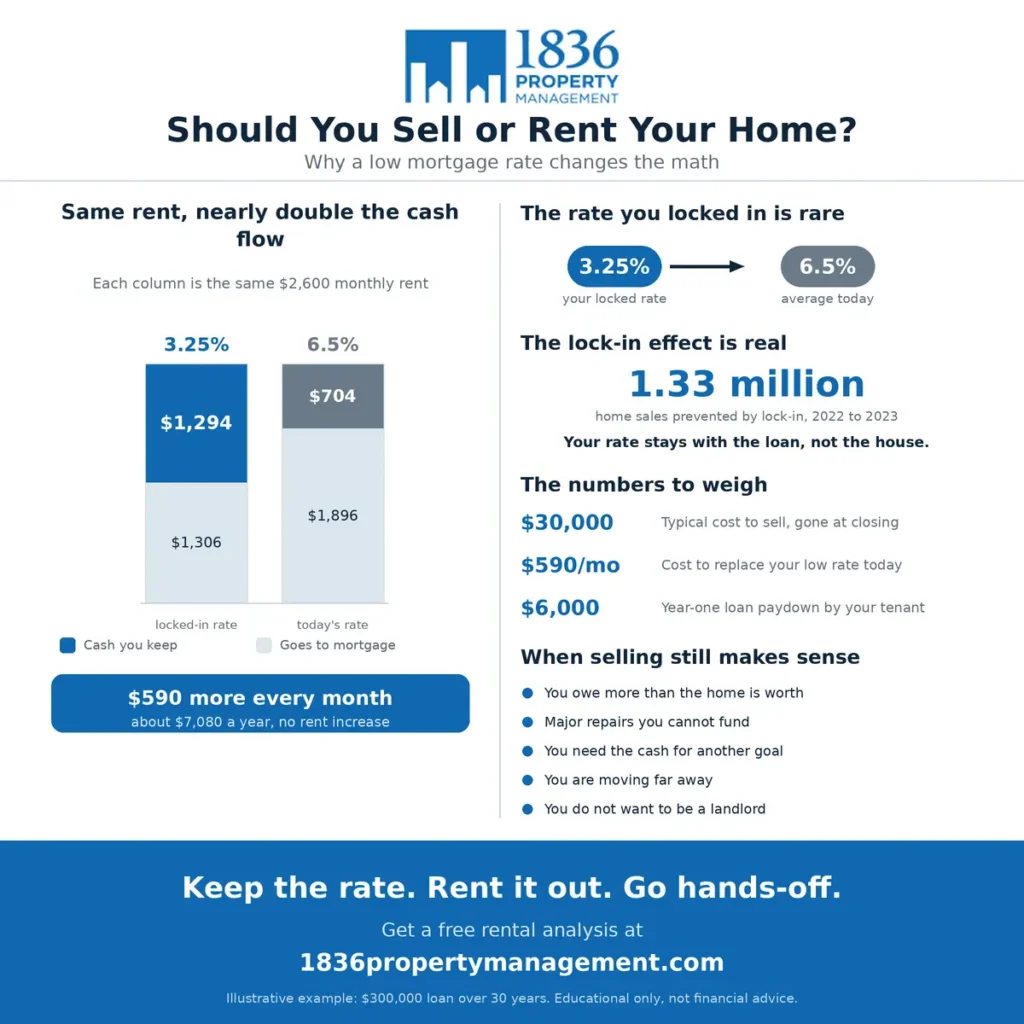

When you hold a loan with a rate far below today's rates, selling means walking away from cheap money. Economists call this the mortgage rate lock-in effect. It is a powerful force. In fact, a Federal Housing Finance Agency study found that every one point that market rates sit above your original rate cuts the chance of a sale by about 18%. That same study estimated the lock-in effect prevented about 1.33 million home sales between mid-2022 and the end of 2023.

Here is the key point that many owners miss. Your rate is tied to your loan, not to whether you live in the home. So you can keep the loan and its low rate in place while the property becomes a rental. As of mid-2026, the average 30-year fixed rate sits near 6.5%. That means a 3% or 4% loan is like a discount that no new buyer can get today.

Should I Sell or Rent My House? Look at the Real Numbers

To make a smart choice, you need to weigh three things: what it costs to sell, what your low rate is worth, and what you can earn by renting. Let us take them one at a time.

What It Costs to Sell

Selling is not free. On a $450,000 sale, plan for roughly 5% in agent commissions plus about 2% in closing, title, and prep costs. That adds up to close to $30,000 gone at the closing table. You only pay that once, but you never get it back. In our experience, owners often underestimate this number until the final settlement sheet arrives.

What Your Low Rate Is Really Worth

Now look at the value of your rate. Say you owe $300,000 on a 30-year loan at 3.25%. Your monthly principal and interest is about $1,306. To borrow that same $300,000 today at 6.5%, the payment jumps to about $1,896. That is roughly $590 more every month for the exact same debt. Over 10 years, replacing your loan would cost more than $70,000 in extra financing. So your low rate is quietly saving you that money right now, month after month.

Same Rent, Nearly Double the Cash Flow

Here is where the advantage really shows up in your bank account. Picture two owners with the same home, both renting it out for $2,600 a month. The only difference is their mortgage rate. The first owner locked in 3.25%, so the loan payment is about $1,306. The second owner bought today at 6.5%, so the payment is about $1,896. After the mortgage, and before other expenses, the low-rate owner keeps about $1,294 each month, while the owner paying today's rate keeps only about $704. That is nearly double the cash flow from the exact same rent.

The reason is simple. The rate is the one thing that changes here, and it works in the low-rate owner's favor month after month. In this example, the low-rate owner has about $590 more in monthly debt-service cushion before taxes, insurance, repairs, vacancy, management fees, and income taxes. Many core ownership costs still apply, but taxes, landlord insurance, maintenance, vacancy, and management should all be reviewed before you decide. Over a year, that $590 cushion adds up to about $7,080, and you never had to raise the rent by a single dollar to earn it. Better yet, with a great property manager running the show, you barely had to lift a finger either.

What You Gain by Renting It Out

When you keep the home as a rental, a few things can build wealth at the same time. First, your tenant pays down your loan. In year one alone, about $6,000 of principal gets paid off, and that number grows every year. Second, the home may continue to appreciate over time. If it does, those gains build on the full property value, not just on the equity you hold. Third, you may gain tax advantages. The IRS lets rental owners deduct expenses like mortgage interest, repairs, insurance, and depreciation, and several of these are not available on a home you live in.

Because your payment is locked in low, the rent is far more likely to cover your costs and leave cash left over. If you want a benchmark, here is what a healthy return looks like for a rental. Many owners also choose to hold the property in a business entity for added protection, so it helps to understand when an LLC for your rental makes sense.

Rent vs Sell House: A Side-by-Side Example

Let us put it all together. Imagine you owe $300,000 at 3.25% on a home now worth about $450,000, and similar homes rent for around $2,600 a month. The table below shows how the two paths compare. These numbers are examples to show the pattern, so your own results will vary.

| Factor | Sell now | Keep and rent |

|---|---|---|

| One-time selling cost | About $30,000 gone at closing | Little upfront cost to start renting |

| Your 3.25% rate | Gone for good | Kept, saving about $590 a month |

| Monthly income | None after you sell | Rent covers a low, locked payment |

| Loan paydown | Stops | About $6,000 in year one, paid by your tenant |

| Home value growth | You cash out and step away | May appreciate on the full home value over time |

| Tax perks | You lose rental write-offs | You may qualify for depreciation and deductions |

As you can see, selling hands you a one-time check but ends every future benefit. Keeping the home turns your low rate into years of income and growth. In our experience, the gap between these two paths grows wider the longer you hold.

When Does Selling Still Make More Sense?

Renting is not always the right move, and we tell previous clients the same thing. Selling can be the smarter choice in a few clear cases:

- You owe more than the home is worth, or you have very little equity.

- The home needs major repairs you cannot comfortably fund.

- You need the cash now for another goal, like a down payment or a business.

- You are moving far away and do not want a long-distance rental.

- You simply do not want the responsibility of owning a rental.

Taxes matter too. If you sell an investment property, a 1031 exchange can let you defer capital gains by rolling the money into another property. On the other hand, if this was your primary home, timing affects your tax break, which we cover in the FAQ below. When selling is truly the better fit, that is fine. Our goal is the right outcome for you, not a one-size-fits-all answer.

How Do You Turn Your Home Into a Rental Property?

If renting wins, the next step is turning your home into a rental property the right way. Our step-by-step guide on how to rent out your house for the first time covers the full checklist, but here is the short version. First, set the rent based on real market data, not a guess. Second, decide on your rental type, since the tradeoffs between a short-term vs. long-term rental affect your income and your workload. Third, screen tenants carefully, handle maintenance, and follow Texas rules on leases, deposits, and notices. Finally, keep clean records so tax time is simple. In our experience, these first steps feel big, but they are very manageable with the right support.

Let a Property Manager Handle the Hard Part

Here is the best part of keeping your low rate. You do not have to run the rental yourself. A good manager makes the whole thing hands-off, so you keep the financial upside without the daily work. Not sure what that includes? Here is what a property manager does day to day.

Our team handles marketing, tenant screening, rent collection, maintenance, compliance, and clear financial reporting. You can even track your property's performance in real time from your own dashboard. That way, you always know how your investment is doing. For owners who want a true set-it-and-forget-it experience, our professional property management keeps your home earning while you focus on everything else.

Frequently Asked Questions

Should I sell or rent my house if I have a low mortgage rate?

In most cases, renting is worth a close look. A rate of 3% or 4% is very hard to replace today, and renting lets you keep it while a tenant helps pay down your loan. Selling ends that advantage for good. Still, the right answer depends on your equity, your goals, and whether you want to be a landlord.

Does renting out my house change my mortgage rate?

No. Your rate is tied to your loan, not to whether you live in the home. When you rent the property, your existing loan and its low rate stay in place. That is a big reason the keep-and-rent path can be so valuable.

Is there a “should I sell or rent my house” calculator?

A calculator can help you compare monthly numbers, but it cannot price your home's rent in the real market. Our free rental analysis does that for you. We look at your address, your home's features, and current Austin demand to show what it could earn.

Will renting my house cover the mortgage?

It can, especially when your payment is locked in at a low rate. In our experience, a below-market rate makes positive cash flow much easier to reach. We are happy to run the numbers for your specific property so you know before you commit.

Do I have to tell my lender if I rent out my home?

You should review your loan terms first. Many home loans include an owner-occupancy clause for the first year. After that period, renting is usually fine, but the rules can vary, so check your paperwork or ask your lender to be sure.

How long can I rent my home before I lose the capital gains tax break?

To claim the home sale exclusion, you generally must have lived in the home as your main residence for at least 2 of the last 5 years. Rent it out longer than that window and you may lose the break, so timing matters if you plan to sell later.

The Bottom Line

A 3% or 4% mortgage is a rare advantage, and selling gives it away for good. By renting instead, you keep that low rate, collect monthly income, and let a tenant build your equity while your home has the chance to grow in value. When you are ready, start with a free rental analysis to see exactly what your home could earn before you decide whether to sell. Our team will handle the rest.

This article is for general education. It is not personalized financial, tax, or legal advice. Every situation is different, so please talk with a qualified CPA or attorney before you decide.