Owning rental property in Texas can be a strong long-term investment, but it is also a business with real operational risk. A hail claim can wipe out a year of cash flow. A kitchen fire can trigger months of vacancy. A slip-and-fall can turn into a costly lawsuit. And a single uncovered loss can force you to fund repairs out of pocket.

That is where landlord insurance in Texas (also called rental property insurance) comes in. The right policy is designed for non-owner-occupied homes, and it helps protect three things that matter most to landlords:

- Your property (the building and any landlord-owned items)

- Your income (lost rent after certain covered losses)

- Your liability exposure (injuries and claims connected to the property)

At 1836 Property Management, we help rental owners across Austin and Central Texas protect their investments by reducing preventable claims through maintenance coordination, documentation, and vacancy reduction systems.

What is landlord insurance in Texas?

Landlord insurance is property insurance written specifically for a home (or small residential property) you rent to tenants rather than live in.

Most Texas landlords carry a dwelling policy, often a DP3 (Dwelling Policy Form 3), rather than a standard homeowners policy. A DP3 is structured for rental risks, including tenant occupancy, landlord-owned appliances, and loss of rental income after certain covered events.

Think of it this way: homeowners insurance is for your personal residence, landlord insurance is for a business asset you rent out.

Is landlord insurance required in Texas?

In most situations, Texas does not require landlord insurance by law, but that does not make it optional in practice.

Here is what usually applies for rental owners:

- Not legally required: You can own a rental without a landlord policy, but you are accepting the financial risk.

- Often required by your lender: If you have a mortgage, your loan documents typically require property insurance that meets minimum coverage standards.

- A smart baseline for risk management: Even if the home is paid off, one major claim can eliminate years of gains.

What does landlord insurance typically cover?

Landlord insurance is designed to protect the building, your rental income, and your liability. Exact coverage varies by carrier, property type, and endorsements, but most Texas landlord policies include protections in the categories below.

1) The building (dwelling coverage)

This is the foundation of your policy. It typically covers the physical structure of the rental home, including:

- Roof, exterior walls, framing

- Flooring, cabinets, countertops

- Built-in fixtures

- Plumbing, electrical, HVAC components attached to the structure

Landlord takeaway: This is the coverage that protects your capital investment. Make sure it is based on rebuild cost, not market value.

2) Other structures

Landlord insurance typically covers detached structures on the property, such as:

- Detached garage

- Storage shed

- Fence

- Detached carport

Landlord takeaway: Other structures coverage is often limited to a set amount or a percentage of dwelling coverage. Fences and detached garages are common “surprise gaps,” so confirm your limit.

3) Landlord-owned personal property (limited)

If you provide items for tenant use, many landlord policies can cover them, up to a specific limit.

Common examples:

- Refrigerator, stove, dishwasher

- Washer and dryer (if provided)

- Some window coverings (coverage treatment varies)

Important: This does not cover the tenant’s belongings (furniture, clothes, electronics). That is what renters insurance is for.

4) Loss of rent (fair rental value)

If a covered claim makes the property uninhabitable, many landlord policies can help replace lost rental income while repairs are completed.

Typical situations that may trigger this coverage (depending on policy terms):

- Fire

- Storm damage that forces a temporary move-out

- Certain sudden water damage events

Landlord takeaway: Loss of rent is tied to a covered physical loss that makes the home unlivable. It typically does not apply to nonpayment, eviction, or vacancy due to renovations.

5) Liability coverage (may be included, may require an add-on)

Liability coverage helps protect you if someone claims you are responsible for injury or property damage related to the rental.

Examples:

- A guest trips on an uneven walkway

- A loose handrail results in an injury

- Certain dog-related claims (coverage can vary)

Landlord takeaway: Many owners assume liability coverage is automatically included, but some dwelling policies require endorsements or separate liability coverage. This is one of the most important items to confirm.

Quick checklist to confirm with your insurance agent

When you quote or renew, ask these questions directly:

- Is this policy written for a non-owner-occupied rental?

- Is the dwelling limit based on rebuild cost, not purchase price?

- How much coverage is included for other structures (including fences)?

- What is the limit for landlord-owned personal property?

- Does the policy include loss of rent, and for how long?

- Is liability included, and what are the liability limits?

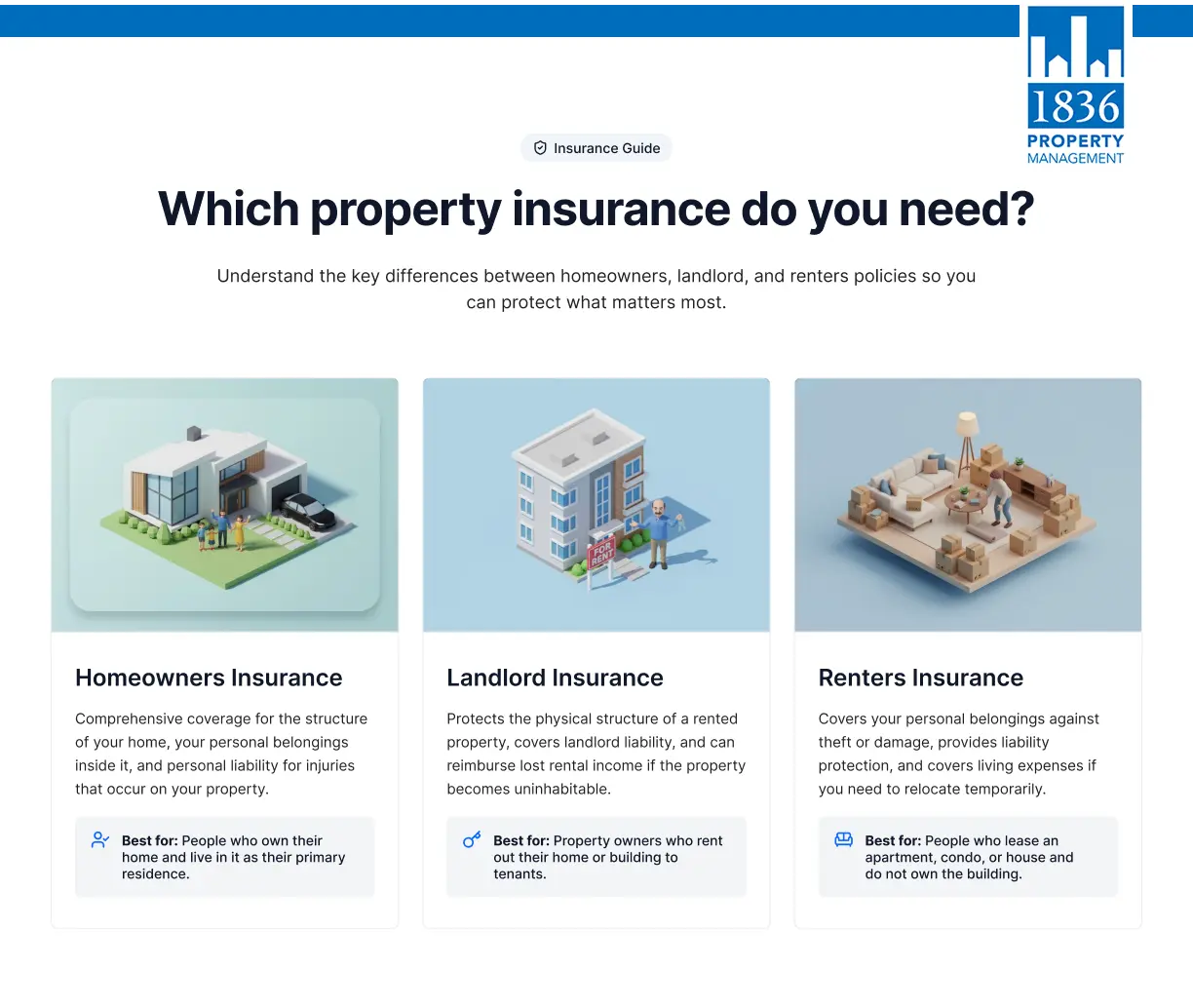

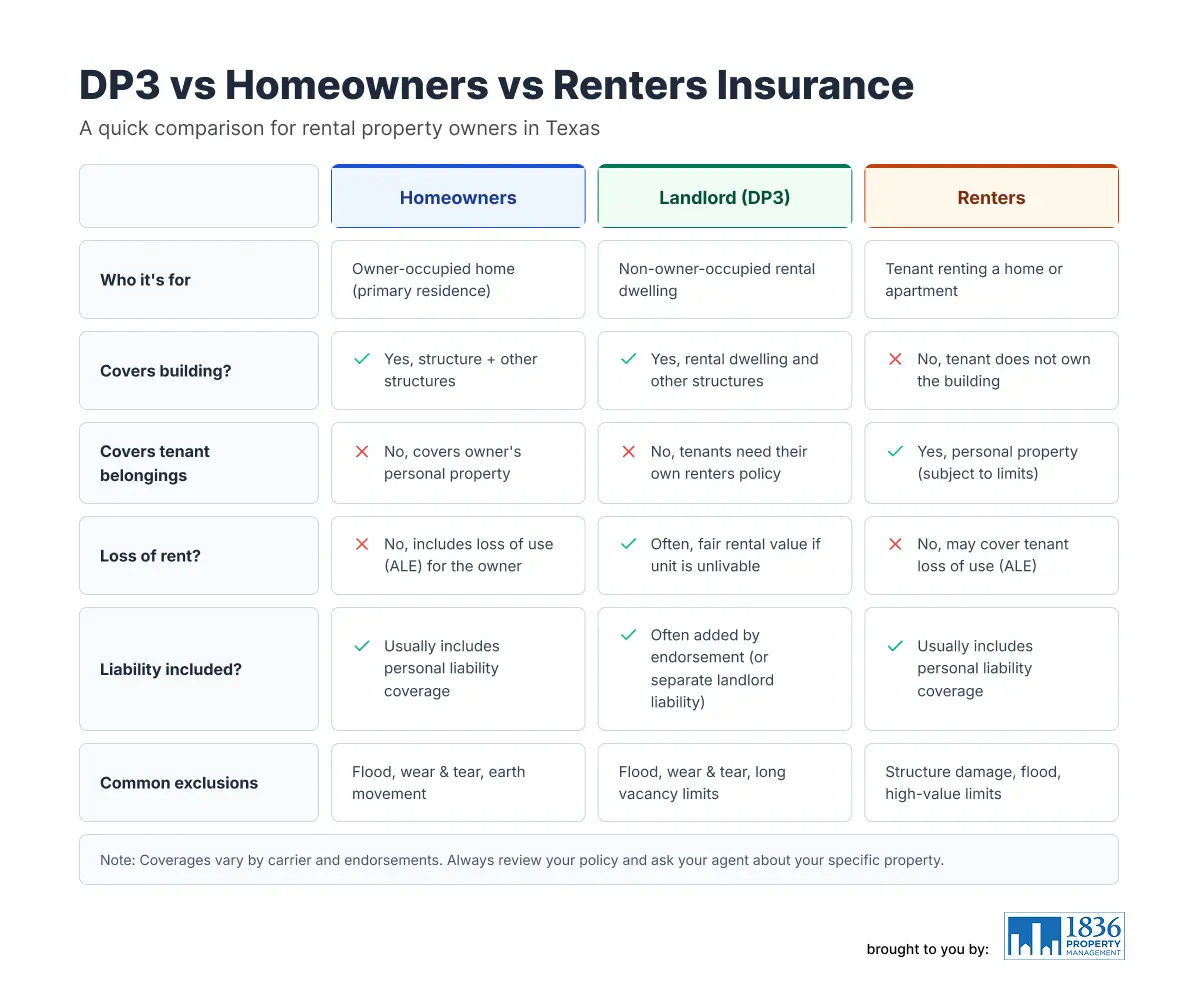

Landlord vs homeowners vs renters insurance

A simple way to think about it:

- Homeowners insurance: for a home you live in

- Landlord insurance (DP policies like DP3): for a home you rent out

- Renters insurance: for the tenant’s personal property and personal liability (not the building)

If you are renting out a home that is insured as owner-occupied homeowners coverage, you may have a claim risk if the policy was not written correctly for tenant occupancy.

*** click the image to make it larger

What landlord insurance usually does not cover (and how landlords handle the gaps)

Most coverage problems happen when a landlord assumes a loss is covered and it is not. Plan for these common gaps:

Tenant belongings

Your landlord policy typically does not cover tenant personal property. Many landlords require renters insurance to reduce disputes and protect tenants.

Flood damage

Flood is commonly excluded from standard property policies and is usually purchased separately.

If your rental is in or near a flood-prone area, ask about:

- NFIP flood insurance, or

- private flood insurance (if available)

Vacancy exclusions (a big one for landlords)

Vacant homes are higher risk. Many policies reduce or restrict coverage if a home is vacant for an extended period. In Texas DP3 language, vacancy rules can affect certain covered perils after extended vacancy (commonly 60 days).

If your rental will be vacant between tenants, during renovations, or while listed, ask about:

- a vacancy endorsement, or

- a policy designed for vacant properties

Wear and tear, maintenance, and long-term leaks

Insurance is not a maintenance plan. Wear and tear, deterioration, and preventable damage are commonly excluded. This is why preventative maintenance and quick response to small leaks matter.

Evictions and nonpayment of rent

Loss of rent coverage typically applies when the property is unlivable due to a covered physical loss, not when a tenant stops paying. Protection for nonpayment is a different category and should be discussed separately with your insurance professional.

*** click the image to make it larger

DP3 policies in Texas: why landlords hear this term so often

Many Texas landlords are told, “You need a DP3,” and there is a reason.

What is a DP3?

A DP3 is a dwelling policy commonly used for non-owner-occupied residential property. It is widely used for single-family rentals and small residential rentals because it aligns better with rental risks than an owner-occupied homeowners policy.

DP3 vs DP1

In general terms:

- DP1 is more basic and often less expensive, but coverage can be more limited.

- DP3 is typically broader for the dwelling portion (with exclusions and policy conditions).

For many landlords, DP3 is preferred because it is designed to be more comprehensive for the building itself, while still allowing customization through endorsements.

Texas-specific issue: windstorm and hail, and when TWIA matters

Texas weather is not one-size-fits-all. A landlord in Austin may focus on hail and wind deductibles. A coastal landlord may need separate windstorm coverage.

Wind and hail deductibles

In many Texas markets, wind and hail deductibles can be significantly different than your standard deductible. Make sure you understand:

- whether wind/hail uses a separate deductible, and

- whether it is a flat deductible or a percentage of dwelling coverage

What is TWIA?

The Texas Windstorm Insurance Association (TWIA) provides windstorm and hail coverage in eligible coastal areas when the private market will not.

If you own a coastal rental, ask your agent how wind and hail are handled so you do not end up with a gap between:

- your main property policy, and

- a separate windstorm policy (when required)

Can’t find coverage? Texas FAIR Plan may be an option

If a property has higher risk factors (location, claims history, condition, or carrier pullbacks), some landlords have trouble finding coverage on the standard market.

The Texas FAIR Plan is designed to provide access to basic property insurance when eligible owners cannot obtain coverage elsewhere. Coverage can be more limited, so it is important to understand what is included and what is not.

How much does landlord insurance cost in Texas?

Pricing depends heavily on:

- location and weather risk

- rebuild cost

- roof age and construction type

- deductible choices (especially wind/hail)

- claims history

- added endorsements (liability, water backup, etc.)

Published averages vary widely, so treat online estimates as a rough reference point, not a quote. The best approach is to request multiple proposals with the same coverage limits and compare them line-by-line.

Practical landlord insurance checklist (Texas edition)

Use this checklist during quoting or renewal.

Coverage structure

- Confirm the policy is written for a non-owner-occupied rental.

- Confirm dwelling coverage is based on rebuild cost.

- Confirm loss of rent is included (and the coverage period).

- Confirm liability coverage and the limits.

Texas risk items

- Ask whether wind/hail has a separate deductible.

- If coastal, ask if windstorm coverage is separate and whether TWIA is involved.

- Ask directly about flood risk and flood insurance options.

Vacancy and turnover planning

- Ask how the policy defines vacancy and what happens after 30 or 60 days.

- If vacancy is likely, ask about a vacancy endorsement.

Documentation and claims readiness

- Clarify documentation requirements (appliances, make-ready work, pre-loss photos).

- List your property manager properly so claims communication is smooth.

Pros and cons of landlord insurance in Texas (landlord view)

Pros

- Helps protect your asset from covered losses

- Helps protect your cash flow through loss of rent coverage (when applicable)

- Reduces liability risk exposure

- Supports lender compliance and refinancing requirements

- Policies can be tailored with endorsements to match your property strategy

Cons

- Often costs more than owner-occupied homeowners coverage

- Policies are detailed, exclusions and vacancy rules require attention

- Some key risks (flood, some water events, vacancy) may require add-ons or separate policies

- Claims documentation requirements can be time-consuming

How 1836 Property Management helps landlords reduce insurance risk

Insurance matters, but reducing the likelihood of a claim is just as important.

1836 Property Management supports rental owners by:

- Coordinating maintenance quickly so small issues do not become large losses

- Keeping documentation organized (work orders, vendor invoices, before-and-after photos)

- Reducing vacancy time with leasing systems and marketing, which can help avoid vacancy-related coverage issues

- Supporting consistent property standards and compliance, which helps reduce liability exposure

If you want hands-off management with systems built for performance, 1836 offers full-service property management across Austin and Central Texas.

FAQ for Texas landlords

Is landlord insurance required in Texas?

Usually no by law, but lenders often require it, and it is a practical safeguard for most rental owners.

Does landlord insurance cover a tenant’s belongings?

Typically no, tenants need renters insurance for their personal property.

Does landlord insurance cover lost rent if my tenant stops paying?

Usually no. Loss of rent generally applies when the unit is unlivable due to a covered physical loss, not nonpayment.

What happens if my rental is vacant for a while?

Many policies restrict certain coverages after extended vacancy. Plan for this during turnover or renovations.

Do Texas landlords need separate flood insurance?

Flood coverage is commonly purchased separately, either through NFIP or a private flood insurer.

What if I cannot get coverage through normal carriers?

Depending on the property and location, options may include the Texas FAIR Plan or TWIA (coastal windstorm and hail).

Final note

This guide is educational and not insurance or legal advice. Coverage varies by carrier, endorsements, and property condition. Always review your policy terms and talk with a licensed Texas insurance professional before making coverage decisions.

If you would like help reducing risk on the operational side (maintenance coordination, inspections, documentation, leasing, and vacancy reduction), 1836 Property Management supports landlords across Austin and Central Texas.